Featuring Machine Learning experts from Cornell, Citi, and more…

You and your colleagues are invited to attend the UBS & CFEM AI, Data & Analytics Speaker Series. UBS Investment Bank is proud to be partnering with Cornell Financial Engineering Manhattan to provide insights directly from practitioners and academics to the next generation of AI, Data & Analytics talent.

All webinars are from 5:30 pm to 6:30 pm ET.

This seminar is free and open to all, but please note that we are restricting the remaining talks to online attendance only. Registration is required (please RSVP here). You will receive the webinar link and dial-in info upon registration (the confirmation email will come from no-reply@zoom.us).

Abstract:

We apply text-mining techniques in earnings call transcripts to extract meaningful features that capture management and investment community signals. Using a corpus of transcripts of earnings calls for global companies from 2010 to 2021, we create fundamentally driven features spanning document attributes, readability, and sentiment on different sections of the transcripts. We test the efficacy of these features in predicting the future stock returns of companies and find that there are opportunities for investors to use these signals in stock selection. Specifically, we find that readability and sentiment-based techniques can enhance an investor’s ability to differentiate amongst outperformers and underperformers and these results are robust across market capitalization as well as investment universes (US Large Cap, US Small Cap, World ex-US, and Emerging Markets). We also introduce methods to create more robust sentiment features for active and systematic investors. By analyzing the performance patterns of the various call participants, we find evidence that the analyst questions may contain more information than the executive sections. Finally, we observe that sentiment features derived from context-driven deep learning language models like BERT are promising and may have more efficacy than bag-of-words approaches.

Speaker Bio:

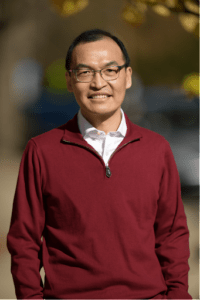

Yuyu Fan is a Senior Data Scientist at AllianceBernstein. She leverages statistical, machine learning, and deep learning models to distill insights from financial data. Yuyu leads projects leveraging the latest NLP techniques to generate investment signals for AB’s portfolio management teams using text data. She also engages with AB’s client teams to develop models and actionable insights to improve client engagements and the sales process. Prior to joining the firm in 2018, Yuyu worked at College Board as a psychometrician intern for two years, using machine learning models to monitor test validity, reliability, and security. Yuyu holds a BA in sociology from Zhejiang University (Hangzhou, China), MAs in sociology and psychology from Fordham University, and a Ph.D. in psychometrics and quantitative psychology from Fordham University.

We hope to see you online!

**Please excuse any duplication of this announcement

If you are interested in our past seminars, you are welcome to subscribe to our YouTube Channel and watch our videos!

Past Events

September 13, 2022

Speaker: Ciamac Moallemi (Columbia)

Title of Presentation: Liquidity Provision and Automated Market Making

September 16, 2022

Future of Finance Conference

Upcoming Events

November 8, 2022

Speaker: Kevin Webster

Title of Presentation: TBD

November 29, 2022

Speaker: Chakri Cherukuri (Bloomberg)

Title of Presentation: TBD